Today, in a context in which environmental challenges are increasingly pressing and social awareness is growing, it is evident how nature directly affects the availability of resources, production chains and, consequently, corporate business. A concrete example of this dynamic is provided by Illy's research on Arabica coffee. With the forecast of a 50% reduction in the land suitable for Arabica coffee cultivation by 2050, Illy has collaborated on a project to sequence the genome of Arabica coffee, making the results available to growers. In this way, producers can adapt plants to the challenges of climate change, such as rising temperatures, droughts and floods. In the face of scenarios like this, it becomes essential to recognize nature as a stakeholder within corporate decision-making processes. However, this integration raises two main challenges:

- Conflict between environmental and social interests and financial goals: how to balance economic and environmental needs?

- Lack of formal recognition of "Nature" as a stakeholder in financial reporting systems, preventing it from being treated as an element to be "remunerated" or included in the distribution of the value created.

The latter barrier could be overcome through regulatory interventions that impose environmental compensation obligations, thus pushing companies to internalize the costs and responsibilities deriving from their activities.

A new model: the Sustainable Value Table (SVT)

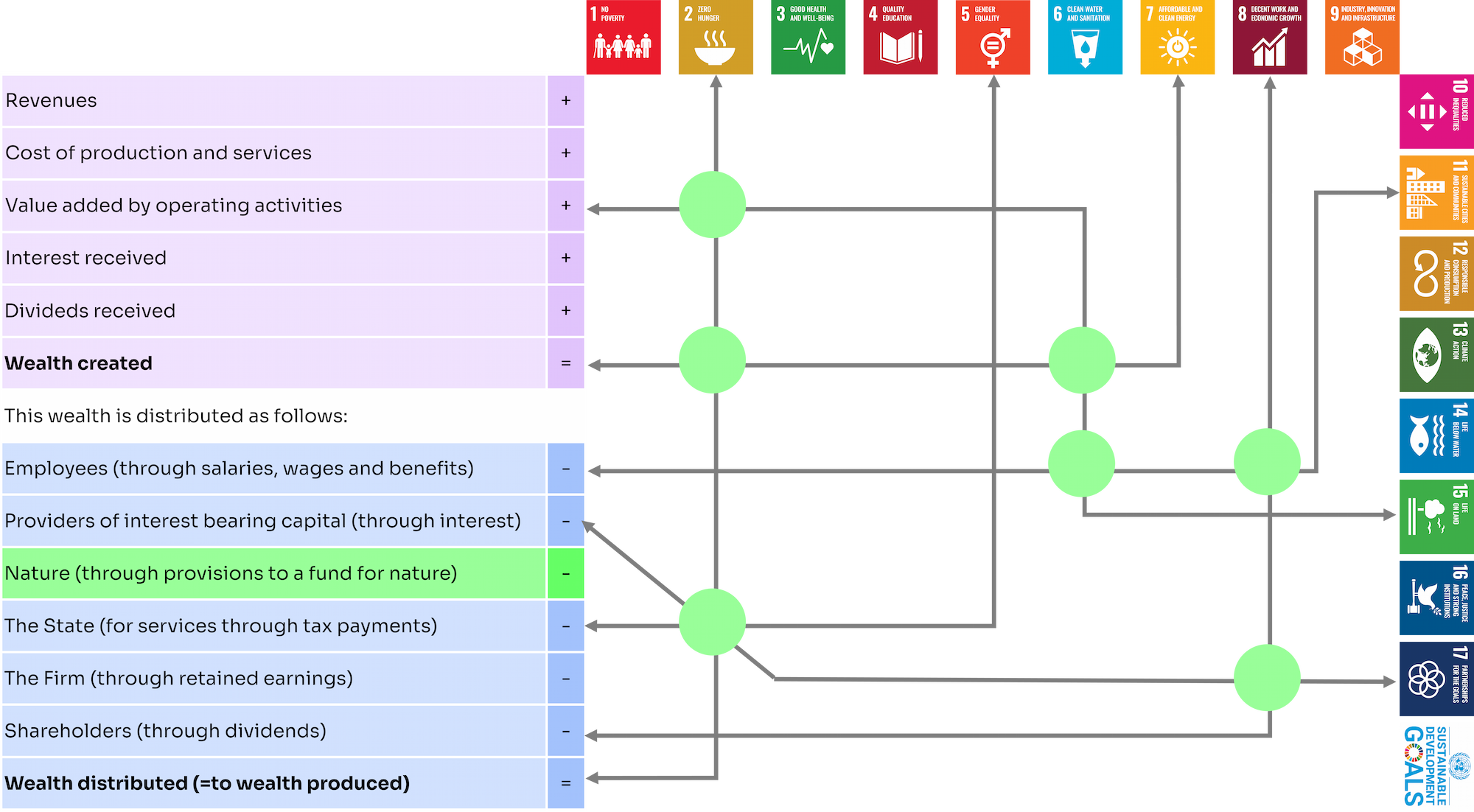

The answer to these challenges comes from the study Calculating Sustainability – Can Accounting Save the World?, which proposes the Sustainable Value Table (SVT), an accounting model designed to link the financial dimension (represented by the income statement expressed in terms of value added, in which "Nature" as a stakeholder is also present) to the non-financial dimension expressed through the Sustainable Development Goals (Sustainable Development Goals, SDGs). This SVT matrix, shown in the following figure, promotes double materiality, recalled by the ESRS principles, guiding companies towards more sustainable and holistic decisions.

Regardless of the sector in which the company operates, the SVT matrix represents a tool to understand how business activities can contribute to one or more SDGs.

A practical approach to sustainability

In practice, the company can classify the SDGs into two main categories:

- Increased positive externalities

- Reduction of negative externalities

To date, the too broad definition of the SDGs makes it difficult to associate them with specific budget items. For this reason, SVT is mainly used as a qualitative tool to map the current state of value creation, identify areas for improvement and guide business strategies. SVT supports the optimisation of short-term adjustments in value distribution to offset negative impacts from value creation.

A possible future for sustainable reporting

Although today the Sustainable Value Table is not yet a mature tool to be used as a reporting method, it already represents a valuable resource for guiding corporate policies, investments and sustainability practices. The results that emerged from the use of the SVT matrix could be included in sustainability statements, helping to make the link between the company's activity and its environmental and social impacts more transparent and strategic.