Dynamic Sustainability Report

The solution designed to foster dialogue between companies and stakeholders through modular questionnaires on environmental, social, and governance (ESG) topics.

Why collect sustainability data?

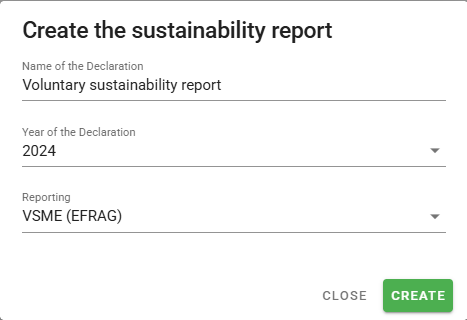

Voluntary Sustainability Declaration

(VSME Standards)

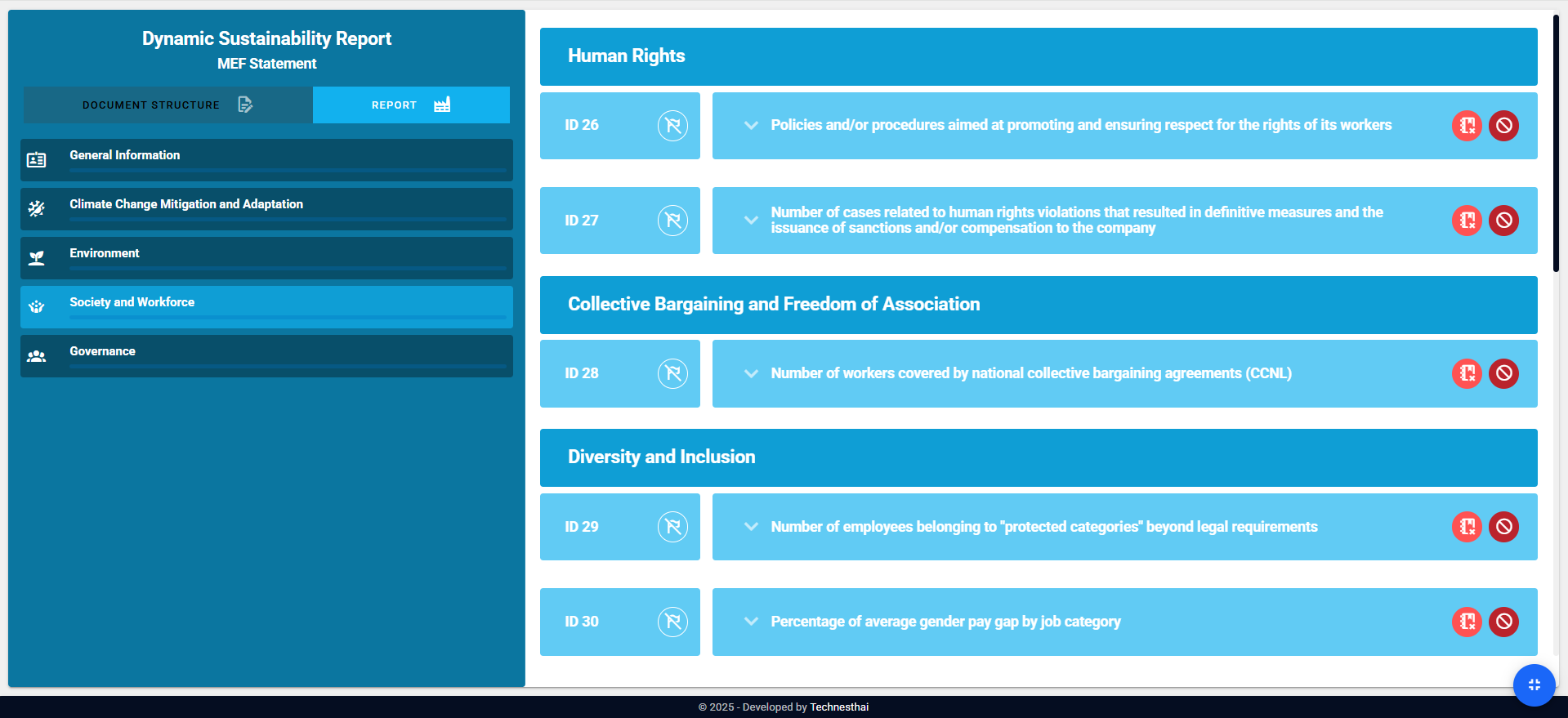

Document for Sustainability Dialogue between SMEs and Banks

Credit Reports & Corporate Resilience

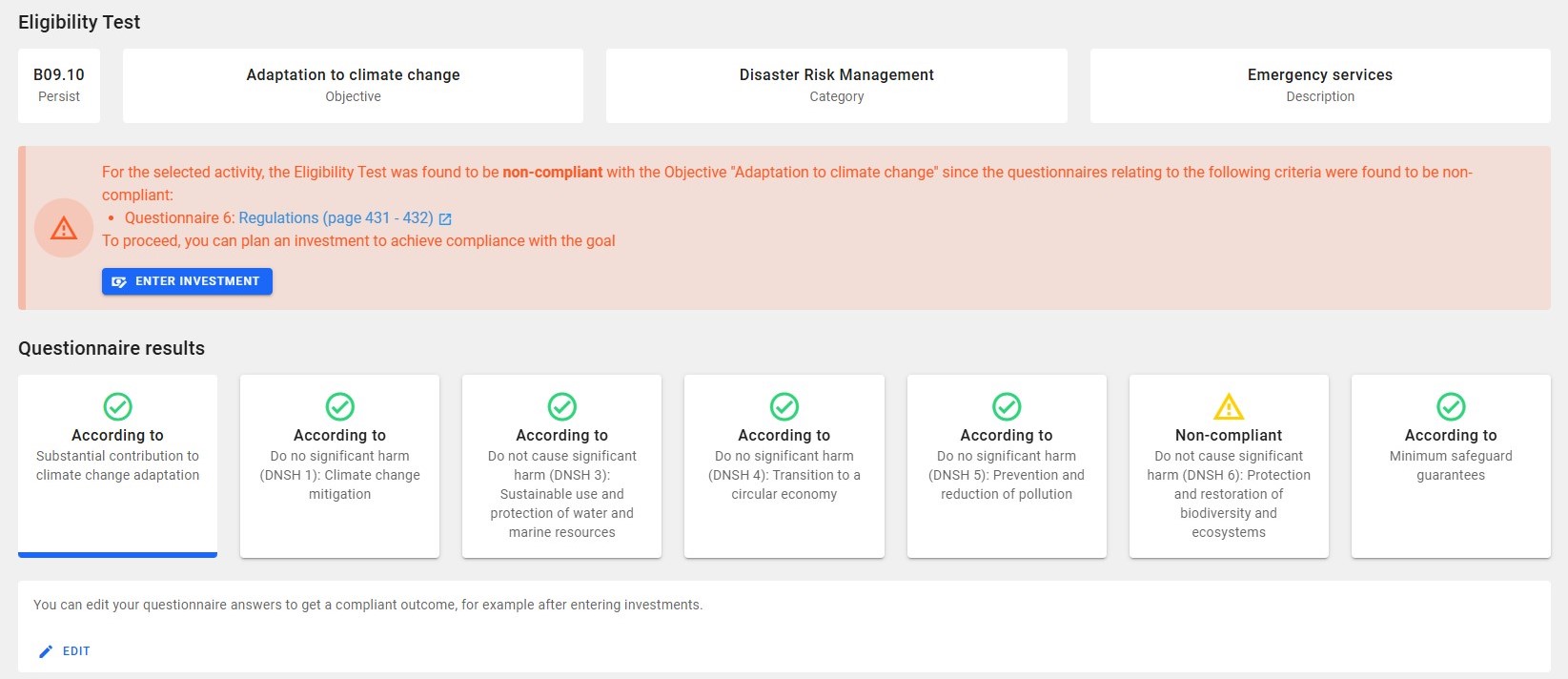

EU Environmental Taxonomy

How is sustainability data collected?

Dynamic Sustainability Report is a SaaS platform designed to simplify and optimize the voluntary sustainability reporting process, reducing time, costs, and complexity.

Optimize your reporting process

The solution guides users in collecting ESG information, taking into account national feautures, to prepare the voluntary sustainability declaration according to European or national guidelines.

Voluntary Sustainability Declaration (VSME Standards)

Through the modular approach, it is possible to prepare your voluntary sustainability declaration for each thematic area:

- General Information

- Environmental Metrics

- Social Metrics

- Governance Metrics

Sustainability Dialogue between SMEs and Banks

The application supports users in completing ESG information according to the thematic areas defined by the Sustainable Finance Committee:

- General Information

- Climate Change Mitigation and Adaptation

- Environment

- Society and Workforce

- Business Conduct

Use Cases

Dynamic Sustainability Report is a tool designed to support SMEs and ESG consultants in various application areas. Below are some examples of use.

European Union Taxonomy

The EU Taxonomy solution allows companies of any size to verify the environmental sustainability level of their economic activities according to EU regulations and to make sustainable investment decisions. Using their ATECO code, companies can consult environmental objectives and, through a dichotomous questionnaire, collect information quickly and easily, supporting them in their reporting obligations.